On February 1, Wolfspeed and ZF announced a strategic partnership to target future SiC semiconductor systems and devices for mobility, industrial and energy applications. One way it will achieve this is by building significant SiC production capacity in Europe.

Wolfspeed’s new facility in Germany will be the largest 8-in. dedicated SiC device fab, and the only fab in Europe capable of producing 8-in. SiC wafers at high volume (excluding some SiC-compatible capacity at STMicroelectronics). The move is set to cement Wolfspeed’s leadership in SiC wafers, but also see it target business in the SiC device market, which is currently dominated by European companies.

Yole Intelligence, part of Yole Group has been studying the SiC market since 2003, predicts that global SiC device capacity will triple by 2027 among the top five firms: STMicroelectronics, Infineon Technologies, Wolfspeed, onsemi and ROHM. The SiC device market will be worth US$6 billion in the next five years, Yole Intelligence’s analysts forecast and could reach US$10 billion in the early 2030s. In 2022, the leading SiC players at device and wafer levels are shown in the graph above.

Power SiC market evolution and technical trends are well detailed in Yole Group’s products: Power SiC/GaN Compound Semiconductor Market Monitor, Power SiC, Toshiba 3rd Generation SiC MOSFET, Automotive Low-Voltage Si MOSFET Comparison 2022 and more.

8-in. production dominance

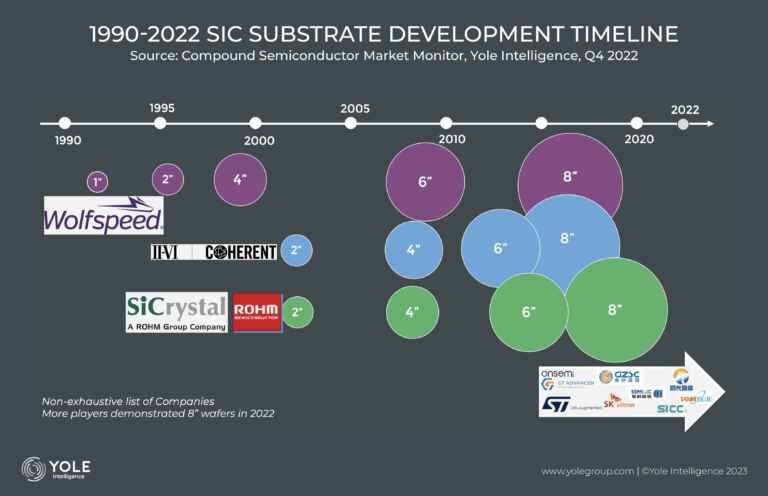

Through its existing fab in New York, Wolfspeed is the only company in the world that can produce 8-in. SiC wafers in volume. This dominance will continue for the next two-to-three years, until further companies start to build capacity – the earliest being STMicroelectronics’ 8-in. SiC facility set to open in Italy in 2024-5.

The U.S. leads in SiC wafers, where Wolfspeed is joined by Coherent (II-VI), onsemi and SK Siltron css, which is currently expanding its SiC wafer production facility in Michigan. Europe, on the other hand, has a strong leadership in SiC devices.

“European players such as Infineon Technologies and STMicroelectronics maintain this leadership by multi-sourcing 6-in. wafers from the U.S., Europe and China. But as Wolfspeed expands into Europe with an in-house, exclusive supply of 8-in. wafers, it is becoming more crucial for European companies to be able to source larger diameters. STMicroelectronics’ Italian facility will help to create some supply, but Wolfspeed’s immediate dominance gives it a competitive advantage in gaining more business in SiC devices,” said Poshun Chiu, technology and market senior analyst specializing in compound semiconductor and emerging substrates at Yole Intelligence.

Larger wafer sizes are beneficial because a greater surface area drives up the number of devices a single wafer can yield, which in turn decreases cost at the device level. As of 2023, we’ve seen multiple SiC players demonstrated 8-in. wafers for future production.

6-in. wafers are still important

“However, other major SiC players are deciding not to focus solely on 8 in. and are placing strategic importance on 6-in. wafers. While moving to 8 in. is on the agenda of many SiC device companies, the expected ramp-up of the more mature 6-in. substrate – and subsequent increase in cost competition, likely to negate the cost benefit of 8 in. – is resulting in SiC players concentrating on both sizes for the future. Companies such as Infineon Technologies, for example, are not making immediate moves to boost 8-in. capacity, in a contrasting strategy to Wolfspeed,” said Ezgi Dogmus, PhD., team lead analyst in compound semiconductor and emerging substrates activity within the power and wireless division at Yole Intelligence.

Wolfspeed, however, is unique from other companies involved in SiC in that it is solely focused on that material. Infineon Technologies, onsemi and STMicroelectronics, for example – who are leaders in the power electronics industry – also have successful businesses within the Si and GaN markets. This factor also plays into the contrasting strategies of Wolfspeed and other major SiC players.

Opening up further applications in U.S.

Yole Intelligence considers the automotive sector to account for 70 to 80 percent of the SiC device market in 2023. As production capacity ramps up, SiC devices will become more accessible for industrial applications such as electric vehicle chargers and power supplies, as well as green energy applications such as photovoltaics and wind power. Automotive will still be the main driver, however, with its market share not expected to change in the next 10 years, Yole Intelligence’s analysts predict. This is especially the case as regions bring in electric vehicle targets to meet climate targets in the current and near future.

Other materials such as Si IGBT and GaN on Si could also be an option for OEMs in the automotive market. Companies such as Infineon Technologies and STMicroelectonics are exploring these substrates, particularly as they provide high-cost competitiveness and do not need dedicated fabs. Yole Intelligence has been watching these materials closely over the last few years and sees them as potential competition for SiC in the future.

Wolfspeed’s expansion into Europe with 8-in. production capacity will no doubt see it target the SiC device market currently dominated by Europe. But with differing strategies at play it will be interesting to see how the market evolves in the coming years.