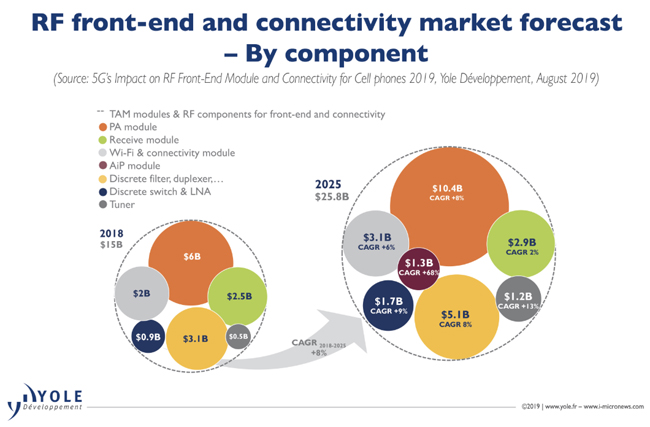

This is a summary taken from the recent release by System Plus Consulting’s partner, Yole Développement (Yole). Yole projects an 8% CAGR between 2018 and 2025 for the RF front-end market. At US$15 billion in 2018, the industry is projected to reach US$25.8 billion by 2025, according to Yole. The team put together a comprehensive look at the RF Front-end market and the breakdown of various device manufacturers market share and participation in key smartphone platforms by analyzing the teardown of 50 smartphones in the market.

The main phone manufacturers differentiate from each other in the RF field by adopting either an integrated or a discrete approach. In the former segment, market leaders Samsung and Apple, along with smaller OEMs like Sony, LG, Google, and ZTE, are moving towards integration with complex RF modules from Broadcom, Skyworks, Qorvo, Qualcomm, and Murata. “Integrated” players prefer to focus on the user experience with innovative features like “Face ID”, wireless charging, AI camera, gesture recognition, and the human machine interface, thus leaving most of the RF front-end’s complexities to the RF module makers.

In System Plus Consulting’s comparative analysis, Stéphane Elisabeth explains: “From the selected smartphones, most of the components are supplied by Qorvo in number. Moreover, based on the overall devices we identified, the majority is led by the antenna tuner which have 24 % of the share in the function distribution followed by the discrete filter, followed by Murata with 23 %, and Qualcomm with 19 % of the design win mainly due to the discrete filters and the chipset design.” The last three suppliers, Infineon Technologies, NXP and Wisol, have a very small fraction of the design win share because of their single appliance in the smartphones (Switch/LNA, LNA, Discrete filter).

A detailed description of System Plus Consulting comparison is available on i-Micronews, within the RF devices & technologies report collection. “The RF front-end leaders still share 81% of the market, with Murata leading ahead of Skyworks and Broadcom”, details Cédric Malaquin, Technology & Market Analyst, RF Devices & Technologies at Yole. And he adds: “Qualcomm, which is already strong in LNAs, is catching up along with Qorvo, thanks to the aggregation of TDK Epcos’ filter business. Established companies like Infineon Technologies, Sony, Taiyo Yuden, NXP, and Wisol also possess a market slice.” These companies generally have manufacturing capabilities for supplying LNA, switches, tuners, and filters, which gives OEMs an alternative to the RF front-end market leaders. Moreover, a variety of fabless companies are emerging, especially in China. Unisoc RDA, Airoha, Richwave, Smarter Micro, Huntersun, and Maxscend are several examples of players scoring more and more design wins amongst the Chinese OEM brands.

Obviously, foundries and design houses support this business model for compound semiconductor, silicon, and even acoustic wave filter. For each player in the RF front-end, a market share breakdown by component is included in Yole’s report, along with a company outlook describing each player’s development strategy for 5G and beyond. All year long, System Plus Consulting and Yole Développement publish numerous RF Electronics reports.