Yole Développement just released a comprehensive report on the RF power device market and here are the highlights from their article. In 2016, telecom operators cut investment so there was a downturn in the market. By year-end, estimates the total RF power semiconductor market was close to $1.5B for all applications above 3W. They expect the market to recover in coming years due to increasing demand for telecom base station upgrades and small cell implementations. Overall market revenue could potentially increase 75% by the end of 2022, posting a CAGR of 9.8% from 2016-2022.

They state that we are at the threshold of completion of 4G networks and beginning the transition to 5G soon (I think 4G still has a ways to go will overlap the 5G implementation). While there are still questions, some things are for sure: the new radio network will require more devices and higher frequencies. Chip providers therefore have a tremendous opportunity, especially RF power semiconductor manufacturers. Yole estimates the market size of telecom infrastructure including base stations and wireless backhaul accounts for about half of the total market size. It will continue growing fast at an expected 12.5% CAGR for base stations and 5.3% CAGR for telecom backhaul over 2016–2022.

Defense applications are also providing good opportunities for RF power devices as there’s a trend of replacing old vacuum tube designs with solid state technologies exploiting GaAs and GaN. These new technologies provide better performance and reduced size as well as robustness in various use cases, and are gradually taking more market share. Yole estimates this market segment’s revenue to increase around 20% by 2022 with a CAGR of 4.3% for 2016-2022.

Compound Semiconductors

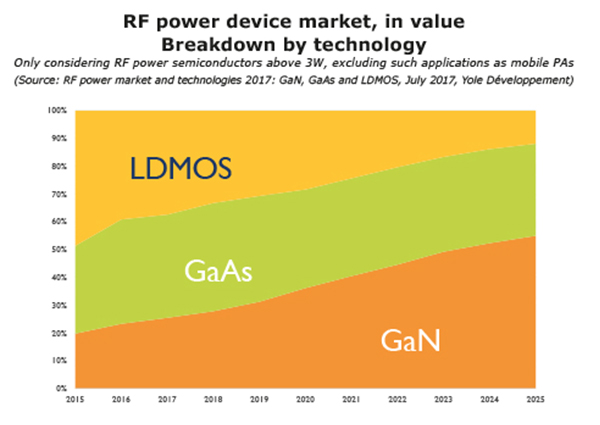

Technology is evolving with GaN device revenues representing more than 20% of the overall market. GaN is replacing LDMOS in telecom macro base stations, vacuum tubes in radar and avionic applications, as well as other broadband applications. GaN’s increased implementation in base stations and wireless backhaul stems from the growing the demand for data traffic and higher operating frequencies and bandwidths. In future network designs, new technologies like carrier aggregation and massive multiple input, multiple output (MIMO) will actually put GaN in a superior position compared to existing LDMOS with its high efficiency and broadband capability.

There will still be a very solid market share that LDMOS can handle with its maturity and low cost. Also, the development of the RF energy market also potentially offers future prospects for LDMOS (and potentially GaN).

GaAs will also secure a considerable share in the industry with its implementation in defense and CATV markets. Thanks to the mobile cellular industry, GaAs technology is very mature and accessible in the market. This will allow a smooth transition into solid-state technology in several military applications.

For the next 5-10 years, Yole envisions that GaN will gradually replace LDMOS and become the major technology for RF power applications above 3W. GaAs will keep its share due to its proven reliability and good cost performance ratio. LDMOS will decline and drop to around 15% of the overall market size.

The fight for Market share

As the developing trends become ever clearer, RF power players are investing and hoping to win the competition to be the leader in next generation technology. Major LDMOS players like NXP, Ampleon and Infineon are gaining access to GaN technology by using external foundries. Meanwhile, traditional GaAs players have been investing in GaN technologies. Some have succeeded in converting their production capacity allowing them to adapt to GaN technology and take the lead in today’s market. Pure GaN players like Wolfspeed are on one hand supplying major LDMOS players, hoping to grow the market together. On the other hand, they are trying to ensure their leading place in GaN technologies with better processes and larger wafer production capacities.

Today’s leading RF power players are still the leaders in the LDMOS area. However, when GaN devices become dominant in the future, the leaders will become those who hold the largest GaN market share. The current top GaN RF players mostly have GaAs experience and there’s only one pure GaN player, Wolfspeed. Under these circumstances, Infineon’s acquisition offer for Wolfspeed seemed beneficial; however, the US government denied the deal going through. This would have given Infineon a dominant position in the future GaN industry, providing it with a complete portfolio in both RF and power applications. At the same time, the legal action initiated by MACOM against Infineon concerning GaN on Si patents caused a commotion in the market. Although it is still ongoing, there will likely be more confrontations in the future as they both vigorously want to defend their positions. The next few years will be interesting.