The power electronics market continues to grow due to government regulations, the demand for renewables and the need for increased efficiency. In 2022, the total power electronics market was worth US$20.9 billion, including discretes and modules. It is expected to grow to US$33.3 billion by 2028.

Worth US$14.3 billion in 2022, the discrete market is expected to reach US$18.5 billion by 2028. The main applications driving this growth are x electric vehicle (xEV), DC charging infrastructure and automotive. Consumer remains the largest market for discrete devices even if it is in decline. In parallel, the module market is pushed by xEV and renewables applications. It includes both photovoltaic and wind. According to Yole Intelligence, this market should reach US$14.8 billion by 2028.

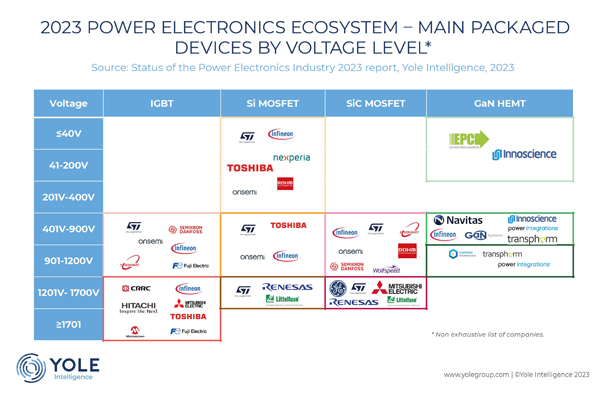

Ana Villamor, Ph.D., team lead analyst, power electronics at Yole Intelligence, commented, “The power device market is split into three different materials: Si, SiC and GaN. Without doubt, silicon is the major part of this market, though SiC is gaining momentum. At Yole Intelligence, we see the growing demand for modules for xEV. In parallel, GaN’s main application will continue to be consumer power supplies.”

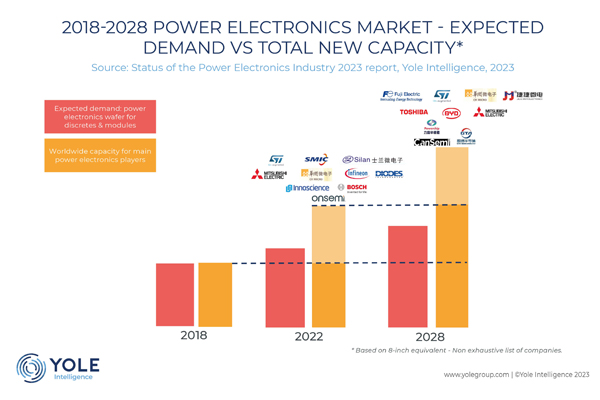

In the long term, total wafer production is increasing alongside the growing power electronic device demand from renewables, automotive and industrial applications. To meet this demand, silicon wafers for power applications will grow to about 47 million 8 in. equivalent wafers per year. Meanwhile, wafer players are focusing on 12 in. SiC’s transition to 8 in. is taking place, and in the coming years, this will take a greater share of the market.

Yole Intelligence has released its annual power electronics report, Status of the Power Electronics Industry 2023, which provides an overview of and update on each power electronics market’s forecast and technology trend, from wafer level to inverter level for each different segment. This analysis closely examines the status of the entire power electronics market, updating the various forecasts from the previous edition. It identifies the dynamics of each component type, from wafers to MOSFETs, IGBTs, power modules, converters, etc. This report presents an overview of the market shares of the power electronics market by material types (Si, SiC, GaN) and explores the market shares of the different component types and materials. The main power applications, relevant market trends and their impact on the evolution of technology are also well analyzed.

Today, China is the largest buyer of power components, followed by Asia/Pacific and Europe. New growth areas, previously less active in semiconductor manufacturing, are found where major companies are investing to supply Asia, other than China, such as Malaysia, Vietnam and Singapore.

A detailed look shows that the silicon wafer market is dominated by five leading players, with 88 percent of the market. The three major players are Sumco, Siltronic and Global Wafers. Most of the manufacturers are in Asia/Europe. At the device level, the top manufacturers are pushing the three different device technologies: Si, GaN and SiC. “We have noticed that a few players pushing GaN have stepped back on R&D to wait for a market increase before investing further, such as onsemi and Alpha and Omega,” added Ana Villamor from Yole Intelligence.

From the manufacturing side, China remains the leader in investments for manufacturing expansion in 300 mm, as well as in 200 and 150 mm. Main power integrated devices manufacturers (IDMs) and foundries are constructing/expanding 300 mm lines. Infineon Technologies, Bosch, Toshiba, Nexperia, etc., are part of the ecosystem. A few 200 mm lines are being built worldwide, and 150 mm lines are being re-furbished to 200 mm. Apart from that, Wolfspeed, Infineon Technologies, CRCC, etc., are among the list of power IDMs pushing for 200 mm SiC capacity.