Until recently, Ka-Band was the dominant choice for fixed wireless access (FWA) connections and frequency bands up through Q-Band (33 to 50 GHz) were commonly used for wireless xHaul opportunities, the umbrella term describing backhaul, fronthaul and midhaul applications in 5G radio access networks. The ever-burgeoning demand for more and more bandwidth is continually placing pressure on band selection and this has led to the choice of V-Band (centered on 60 GHz) for new FWA installations and E-Band, mostly at 71 to 76 GHz, for xHaul.1 This article provides some background information together with data forecasts addressing the expected progress for these mmWave FWA and xHaul market opportunities out to the year 2030.

INTRODUCTION

When posed with the question regarding the communications links associated with cellular networks, most people would immediately think about fiber-optic cabling. This is because fiber cabling plays an important role in the broadband networks that connect customer premises equipment in homes and businesses. In most situations, fiber is synonymous with broadband. This is hardly surprising considering that fiber cables can have available bandwidth measured in the several terahertz (THz) range.

However, there are notable issues with fiber cables. They typically require permission before physical installation. This often means that the installation requires a considerable planning period. Especially in urban areas, installation often becomes a costly, prolonged effort that involves digging up roads and/or sidewalks as part of the fiber trenching process.

Wireless transmission between radios provides a simpler alternative to the challenges presented by fiber. The bandwidth of this wireless solution is currently measured in GHz, but this is proving to be sufficient for many applications. Despite less signal bandwidth, wireless radios benefit from a faster, less expensive planning and deployment process than fiber networks. Currently, wireless radio networks intended to meet FWA and xHaul requirements operate in mmWave frequency bands to take advantage of the substantial bandwidths and the resulting capacities available in these bands. Within that broad mmWave frequency range, the portion of the unlicensed V-Band centered around 60 GHz has become popular for new FWA installations. The xHaul applications that connect the wireless radio to the core network are using the lightly-licensed E-Band frequency range, mostly in the 71 to 76 GHz portion of the band. The analysis that follows considers only outdoor radio links, as these links have increasingly become the interconnect method for intelligent mesh networks.

SUPPLIERS OF MMWAVE RADIOS

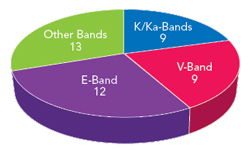

Figure 1 Number of companies supplying radios in various bands.

A wide range of global companies are supplying mmWave radios.2 While not exhaustive, a list of these suppliers includes Ceragon, Filtronic, Movandi, Nokia, REMEC and Siklu. The pie chart in Figure 1 shows a segmentation of the number of companies supplying radios covering various frequency bands in 2023.

The trend is clear. We expect that the number of companies supplying V-Band and E-Band radios will continue to increase along with the shipment quantities as we move forward. By 2030, we expect that the quantity of V-Band and E-Band radio shipments will increase at the expense of K-Band and Ka-Band, along with lower frequency radios.

COMMUNICATIONS SERVICE PROVIDERS (CSPS)

Engalco-Research investigated the following 21 CSPs who operate regionally and globally. The companies that were investigated include A1 Telecom Austria, America Movil, Asia Pacific Telecom, AT&T, British Telecom (including a subset for EE), Charter Communications, KDDI Corporation, KT Corporation, LG Uplus, NTT DoCoMo, Ooredoo, Orange, Reliance Jio, SK Telecom, Telefónica, Telstra, Telus, Three UK, T-Mobile US, Verizon and Vodafone.

Figure 2 Ka-Band and V-Band market shares in FWA applications.

After primary and secondary research on each radio supplier, Engalco-Research built up a numerically detailed assessment of the total addressable market (TAM). We segmented these results into FWA and xHaul applications for wireless radios. The relative market shares for FWA radios are segmented by frequency range in Figure 2.

It is clear from Figure 2 that the market share of the V-Band radios in FWA applications will increase, expanding from a 38 percent share in 2022 to reach an estimated market share of 72 percent by 2030. By contrast, Ka-Band radios experienced a market share of 62 percent in 2022 but Engalco-Research estimates that this share will decline to just 28 percent by 2030. Although V-Band has taken off in many regions, K-Band appears set for substantial market values and annual growth in India due to the current success of the Sivers/Intel/WiSig network consortium. Other Asian, as well as some African, markets may follow with residual market opportunities that will be well-suited for Ka-Band radios beyond 2030.3 In total, we expect that the TAM of these FWA networks will increase to more than $1 billion.

Parsing these data regionally yields the following observations:

- North America (mainly the U.S.) remains the leading regional market over the forecast period. This is driven primarily by AT&T, Verizon and private 5G networks.

- Southeast Asia is consistently the second largest region over the forecast. The biggest regional contributors to this result are Australia, India, Japan and Korea.

- Europe, driven by Western Europe including the U.K., occupies the third position until 2025, when it is passed by the Middle East.

- Markets in the Middle East are relatively small in the earlier years but gather pace throughout the middle and later years.

We also anticipate steady to strong growth rates in these regions:

- For V-Band radios, markets in the Southeast Asia region already exhibit the highest growth rates. We expect these rates to exceed 24 percent over the 2024 to 2027 period.

- Markets in North America continue growing rapidly with a compound annual growth rate (CAGR) averaging more than 20 percent over the full forecast period. We expect that this growth rate will reach 23.5 percent over the 2024 to 2027 period.

- Markets in the Middle East will continue to grow steadily throughout the forecast period and we anticipate this growth rate will accelerate from 2025 onwards.

- In Western Europe (including the U.K.) markets will grow steadily throughout the forecast period.

XHAUL APPLICATIONS

Figure 3 Adoption of various bands for xHaul.

The xHaul network interconnection architectures and opportunities are different from the FWA application. As mentioned, xHaul has become the umbrella term that the industry uses to describe data transport options encompassing backhaul, fronthaul and midhaul, although backhaul remains the most widely known of these applications. Many xHaul networks include fiber-optic cabled systems, but we believe that mmWave wireless is steadily capturing market share in these network applications. This analysis considers K-Band to Q-Band (24 to 43 GHz) and E-Band (mostly 71 to 76 GHz). The market data relating to xHaul is indicated proportionately in Figure 3.3

From Figure 3, the trend of increasing market share as E-Band radios increasingly penetrate these xHaul applications is clear. Engalco-Research anticipates that the share of E-Band radios used in xHaul applications will expand from a 29 percent share in 2022 to an estimated 53 percent by 2030. By contrast, Ka-Band radios occupied a market share of 71 percent in 2022 but Engalco-Research anticipates that this will decline to just 47 percent by 2030.

The geographic segmentation for xHaul is similar to FWA with one exception:

- North America is always the largest region and by a substantial margin.

- Southeast Asia, driven by Australia, India, Korea and Japan occupies the second position and this region also grows rapidly. We anticipate a compounded average growth rate of more than 11 percent overall with the mid-years seeing a CAGR of 12.5 percent.

- The Middle East, driven by the Emirates and the UAE, remains in third position over the forecast.

- Europe is always in the last position in this analysis.

The difference in Europe’s relative position in the xHaul market versus its FWA market position is the exception. This is at least partly due to the relatively strong fiber-optic activity across Europe. Despite this, the E-Band growth rate in this region is 17 percent overall and 22 percent CAGR over the 2022 to 2026 period.

CONCLUSION

Broader 5G network deployments and new applications will increase data traffic. This will place more demands on the transport networks and wireless mmWave radios will become an increasingly important part of both the FWA and xHaul network architectures. In time, even higher frequency bands, like W-Band (75 to 110 GHz) and D-Band (110 to 170 GHz), are likely to be incorporated into operators’ frequency plans to provide the bandwidth to address the ever-increasing demand for data traffic. The shift to higher frequencies from the operators will provide many opportunities for the RF and microwave supply chain and ecosystem.

References

- “5G mobile subscriptions to reach 5 billion by 2028,” Ericsson Mobility Report, November 2022.

- T. Edwards, “Technologies for RF Systems,” Artech House, Boston, Mass., 2018, pp. 9-10.

- “mmWave Radios into Fixed 5G Network Links (FWA and xHaul) – Market Forecasts from 2023 through 2030,” Engalco-Research, Spring 2023.