In the last decade, GaN has become an increasingly important technology for RF applications. The material properties of GaN enable devices with advantages in power density, form factor, breakdown voltage, thermal conductivity, operating frequency, bandwidth and efficiency. Designers have developed device solutions offering very compelling performance characteristics versus competitive semiconductor technologies.

The overwhelming application for GaN devices is power amplifiers (PAs), which take advantage of these benefits. Ongoing product development looks to take advantage of the unique material properties of GaN for other functions, primarily switches and low noise amplifiers. For the near future, however, PAs will dominate RF GaN revenue.

HOW DID WE GET HERE?

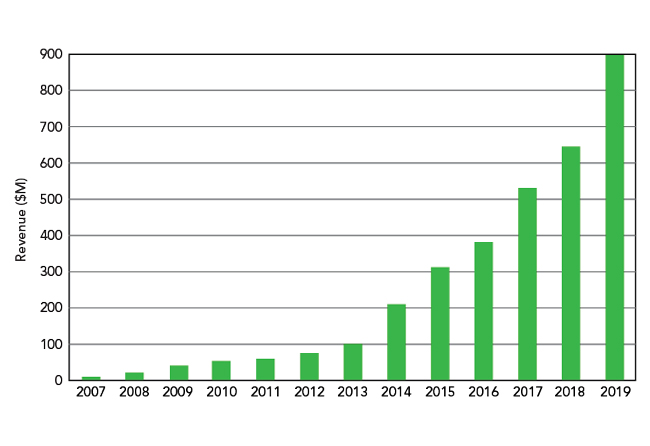

Strategy Analytics began tracking revenue in the RF GaN market in 2007 (see Figure 1). As with many compound semiconductor technologies, defense agencies were instrumental, providing early funding for device and process development, and defense applications served as early adopters of RF GaN devices. During the 2007 to 2013 period, roughly 85 percent of all RF GaN device revenue came from defense applications, with a spattering of GaN device adoption by commercial applications, primarily proof of concept and low volume applications.

Figure 1 RF GaN revenue, 2007–2019.

In 2013, RF GaN device revenue hit an inflection point and the trajectory of revenue growth increased dramatically. Much of the early proof of concept activity came from base station equipment manufacturers evaluating the reliability and performance characteristics of GaN PA devices for future designs. Chinese equipment manufacturers, particularly Huawei, became enthusiastic adopters of GaN technology for next-generation base stations. China’s decision to rapidly deploy 4G LTE capabilities across the entire country fueled the ascension of Huawei as a global leader in base station equipment, and it drove a sharp uptick in RF GaN revenue beginning in 2014. As LTE deployments in China and the rest of the world approach saturation, the revenue growth from 4G has slowed; yet this dovetailed nicely with the emergence of 5G. Moving forward, 5G base station deployments will be the biggest growth engine for commercial RF GaN revenue.

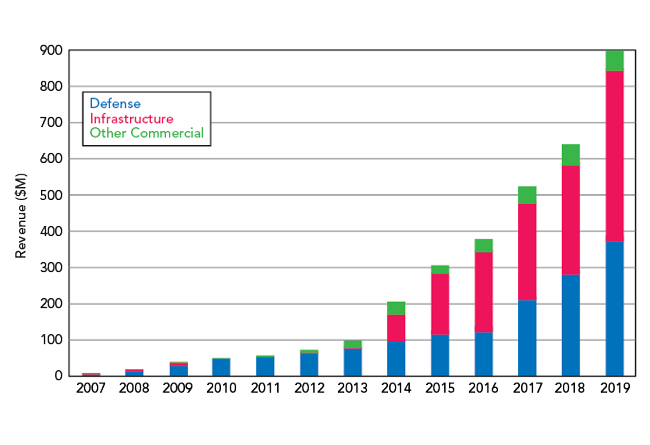

Figure 2 shows the historical segmentation of RF GaN revenue. The importance of the base station segment is clear; what also should be clear is the robust growth of RF GaN revenue from defense applications. Shortly after the spike in 2014, RF GaN revenue in base stations surpassed revenue from defense applications. Note, however, that the revenue from defense has increased 75x from 2007 to 2019 as GaN technology became a key enabler for evolving defense philosophies and battlefield strategies. If not for the extraordinary growth of base station applications, the story of the RF GaN market would have been its growth in defense.

Figure 2 RF GaN revenue by market segment.

The radar market presents the largest opportunity for RF GaN devices. Small, efficient PAs have made radars using active electronically scanned arrays (AESAs) “must haves” for next-generation and major retrofit programs in all domains. These solid-state AESA radars can generate and combine multiple scanning and tracking beams to offer significant performance and reliability advantages over traditional radar architectures.

Like their commercial counterparts, defense communication networks are managing more data traffic and moving higher in frequency in search of bandwidth. Battlefield engagements may involve forces from different nations, with different equipment and waveforms, constrained by the “on the move” aspect of a mission. Satellite equipment on the ground and in space serves as the linchpin for all these communications. The performance characteristics of RF GaN technology enable and supply flexibility for these requirements.

Electronic warfare (EW) is another important application for RF GaN. EW systems rely on broad bandwidth and high frequency ranges to detect targets and avoid detection by hostile forces. These applications require high RF transmit powers to disable or confuse enemy equipment. All these mission requirements fit nicely with the performance advantages of RF GaN.

THE FUTURE

Current geopolitical events are heavily influencing the future of the RF GaN market. To better understand this, we must explore the recent past. Industry insiders say Huawei has been buying electronic parts, particularly for base stations, since 2018. This was triggered by their expectation of tightening U.S. trade sanctions, which led to Huawei being placed on the “entity list,” meaning an export license is required to supply products. Huawei’s base station equipment market share, the purchases to inventory and their affinity for GaN PAs, drove a substantial bump in RF GaN revenue. As illustrated in Figure 2, from 2018 to 2020, RF GaN revenue for base stations more than doubled.

Of course, no discussion of 2020 is complete without noting the COVID pandemic. Global economies are struggling to regain footing, and the recovery has not been uniform. As the pandemic shut down economies, many people and businesses adopted a work-from-home model. Wireless and wireline networks became critical infrastructure. China has said that 5G will be a driving force behind the restart of their economy. As it is unlikely other regions of the world will let China get too far ahead with 5G, expect continuing 5G capital expenditures. Defense spending ties closely to economic growth, raising concerns about the effects of the pandemic on defense spending. As the defense goals of the new U.S. administration are still uncertain, there is also uncertainty about the likelihood of diverting defense spending to broader economic stimulus.

CONCLUSION

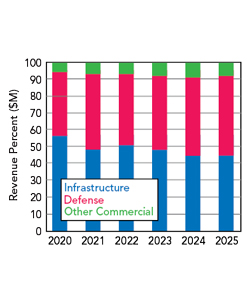

Figure 3 Projected RF GaN revenue by segment.

The adoption of RF GaN devices has increased dramatically in the last several years, with 2020 revenue crossing $1 billion for the first time. Since 2018, RF GaN revenue increased by slightly more than 80 percent.

Challenges will influence the future growth trajectory of revenue. Deployments of 5G base stations will drive revenue growth, but China’s timing for more 5G equipment purchases and how other regions respond to China are uncertainties. Defense spending, tied closely to economic growth, is also uncertain as global economies recover from the pandemic.

Despite these questions, we are still confident that RF GaN revenue will increase over the forecast period. Figure 3 shows our latest market segmentation forecast for RF GaN revenue. We expect steady revenue growth in defense, increasing the market share for this segment. Infrastructure revenue has grown so quickly because of Huawei’s actions that we are forecasting a slight decline in revenue this year until mmWave deployments using GaN reinvigorate revenue growth. While the revenue from the “Other Commercial” segment is small, applications like VSAT, backhaul, CATV and, particularly, commercial satcom are gaining traction. We expect RF GaN revenue will approach $2 billion in 2025, extending the GaN success story.